Since the beginning of this year, due to the continuous impact of multiple complex factors such as repeated epidemics, prolonged geopolitical conflicts, energy shortages, high inflation, and tightening monetary policy, the downward trend of the global economy has gradually become clear, demand-side pressure has become more significant, and the risk of economic recession has increased significantly. .

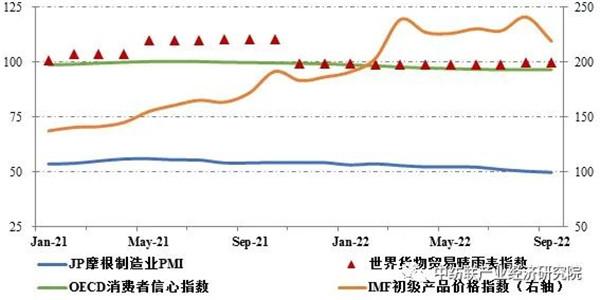

At the end of the third quarter, the global manufacturing industry entered a state of contraction. In September, the J.P. Morgan Global Manufacturing Purchasing Managers Index (PMI) was 49.8, which was the first time since July 2020 that it fell below the boom-bust line. Among them The new orders index is only 47.7, and business confidence has dropped to a 28-month low;

The OECD consumer confidence index has stayed at 96.5 since July, and has been in the contraction range for 14 consecutive months;

The global trade in goods barometer index remained at the benchmark level of 100 in the third quarter. However, according to calculations by the Netherlands Bureau for Economic Policy Analysis (CPB), after excluding price factors, global trade volume fell by 0.9% month-on-month in July and only increased by 0.7% month-on-month in August. .

Affected by tightening liquidity and expectations of economic downturn, global commodity prices gradually fell after August, but the overall price level is still at a high level. In September, the IMF energy price index still increased by 55.1% year-on-year.

Inflation has not yet been fully controlled. Driven by factors such as the slowdown in wage growth, the U.S. inflation rate gradually fell after peaking in June. However, the inflation rate in October was still as high as 7.7%. The euro zone inflation rate At 10.7%, half of the OECD member countries have inflation rates above 10%.

Figure 1: Change trends of major global macroeconomic indicators

Data source: IHS Markit, WTO, OECD, IMF

my country’s macro economy has withstood the impact of the epidemic and The complex and severe external environment and other unexpected factors impacted the Company, and efforts were made to repair the losses. With the implementation of the national economic stabilization package and subsequent policies and measures, the macroeconomic recovery and development momentum is better than that in the second quarter. In particular, the production and domestic demand markets continue to recover, demonstrating good development resilience.

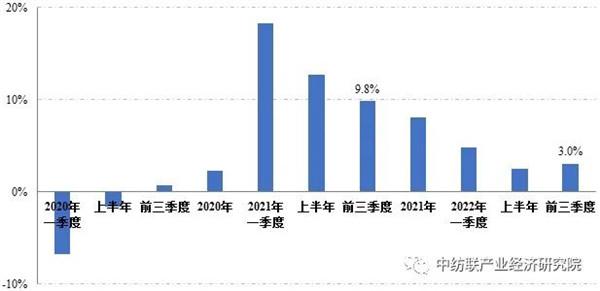

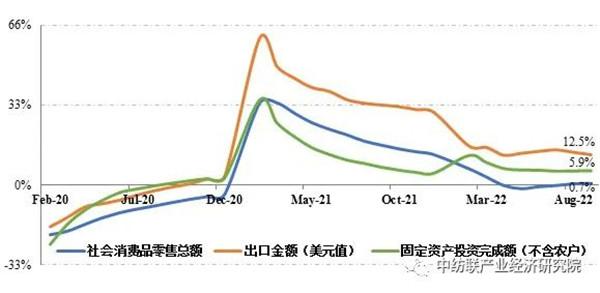

In the first three quarters, my country’s GDP grew by 3% year-on-year, and the growth rate increased by 0.5 percentage points from the first half of the year; the total retail sales of consumer goods and the industrial added value of enterprises above designated size increased by 0.7% and 3.9% year-on-year respectively, and the growth rate Compared with the first half of the year, they rose by 1.4 and 0.5 percentage points respectively.

Exports and investment have basically achieved stable growth. In the first three quarters, my country’s total exports (denominated in US dollars) and fixed asset investment (excluding farmers) increased by 12.5% and 5.9% respectively year-on-year. This is an important step to stabilize the macroeconomic market. Make a positive contribution.

Although my country’s macro-economy has shown a positive momentum of recovery, the profit growth rate of industrial enterprises has not yet turned positive, the manufacturing boom has fallen under pressure, and the foundation for recovery still needs to be further solidified.

Figure 2: my country’s GDP year-on-year growth rate

Data source: National Bureau of Statistics

Figure 3: Cumulative year-on-year growth rate of my country’s main macroeconomic indicators

Data source: National Bureau of Statistics, China Customs

In the first three quarters, the pressure on both supply and demand in the textile industry was superimposed, and the growth rate of main operating indicators slowed down. After entering the peak sales season in September, market orders have increased, and the start-up rate of some links in the industrial chain has increased. However, the overall industry operation situation has not yet shown obvious signs of bottoming out. We strive to improve and demonstrate development resilience, and effectively prevent and resolve various risks. Challenges remain the core focus of the industry.

</p